Explanation:

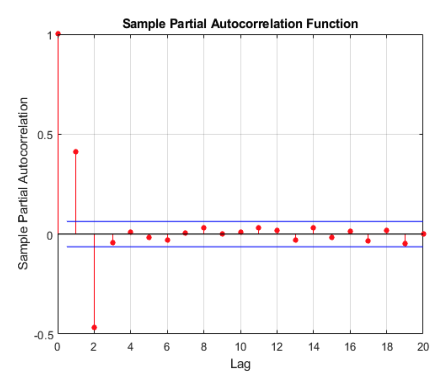

The explanation for the best regression approach for the security, based on the provided Partial Autocorrelation Function (PACF) plot, is that the PACF cuts off after the second lag. This abrupt cessation of the PACF after a specific lag is indicative of an autoregressive process of order 2, which is denoted as AR(2). In time series analysis, an AR(2) process suggests that the current value of the security can be predicted using a linear combination of its two previous values. Therefore, the correct answer is C, AR(2). This approach is suitable for modeling and forecasting the security's performance given the characteristics revealed by the PACF plot.

Ultimate access to all questions.

A market risk manager aims to assess and forecast the performance of a particular security and has already gathered its historical data series. To enhance their evaluation, they consult a colleague from the quantitative analysis team, who provides them with a graph of the Partial Autocorrelation Function (PACF). Based on the provided PACF graph, which of the following regression methods would be most appropriate for analyzing the security's performance?

A

AR(1)

B

MA(1)

C

AR(2)

D

MA(2)