Explanation:

The correct answer to the question is A, which is a 95% confidence interval for the mean return of stock XYZ ranging from -6.69% to 5.19%. To determine this interval, we use the formula for a confidence interval, which is the sample mean plus or minus the t-statistic multiplied by the standard error. In this case, the sample mean monthly return is -0.75%, and the standard error is 2.70%.

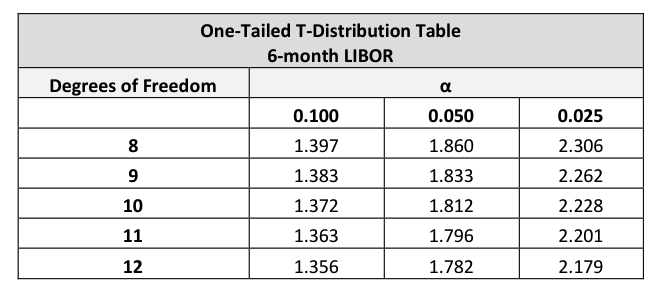

Since we are looking for a 95% confidence interval, we need to find the t-statistic that corresponds to the 0.025 level in a one-tailed test, because we are looking at the interval in both directions from the mean (two-tailed interval). The degrees of freedom (df) are determined by the number of sample observations minus 1, which is 11 in this scenario. From the t-distribution table provided, the t-statistic for 11 degrees of freedom at the 0.025 level is 2.201.

The calculation for the confidence interval is as follows: Lower limit = -0.75% - (2.201 * 2.70%) Upper limit = -0.75% + (2.201 * 2.70%)

Performing the multiplication: Lower limit = -0.75% - 5.943% Upper limit = -0.75% + 5.943%

Converting these to percentages: Lower limit = -6.69% Upper limit = 5.19%

Thus, the 95% confidence interval for the mean return is from -6.69% to 5.19%, confirming that option A is the correct answer. This interval indicates that we can be 95% confident that the true mean monthly return of stock XYZ lies within this range.

Ultimate access to all questions.

No comments yet.

An analyst has analyzed the performance of stock XYZ over a 12-month period and found that the average monthly return is -0.75%, with a standard error of 2.70%. Using a one-tailed t-distribution, the analyst needs to determine the 95% confidence interval for the mean monthly return. Use the provided t-distribution table to calculate this interval.

A

-6.69% and 5.19%

B

-6.63% and 5.15%

C

-5.60% and 4.10%

D

-5.56% and 4.06%