Explanation:

The correct answer to the question is C, which is 7.89%. This is determined by applying Bayes' theorem to calculate the conditional probability that the longevity bond defaults in 1 year given that the market decreases by 20% over the same period. Bayes' theorem is used to find the probability of an event based on prior knowledge of conditions that might be related to the event.

In this scenario, let A represent the event that the bond defaults and B represent the event that there is a 20% decrease in market returns. The formula for Bayes' theorem is:

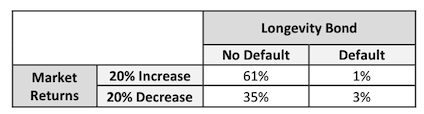

From the provided probability matrix, we can extract the following probabilities:

Plugging these values into Bayes' theorem gives us:

This simplifies to a probability of approximately 7.89%, which is the conditional probability that the bond defaults given that the market has decreased by 20%. This is why option C is the correct answer. The other options represent either incorrect interpretations of the probabilities or the use of unconditional probabilities instead of the required conditional probabilities.

Ultimate access to all questions.

A portfolio manager is studying the relationship between the 1-year default probability of a longevity bond (issued by a life insurance company) and equity market returns. The manager has developed the following joint probability table based on preliminary research:

Based on the table, what is the conditional probability that the longevity bond defaults within one year, given that the equity market declines by 20% over that same period?

A

3.00%

B

4.00%

C

7.89%

D

10.53%