Explanation:

The correct answer is D, which is 0.02801. This is determined by calculating the Dv01 (Dollar Value of 01) of a comparable bond with no embedded options, using the formula:

where is the price of the bond, is the change in yield, and 10,000 is a scaling factor to convert the change in yield to a basis point.

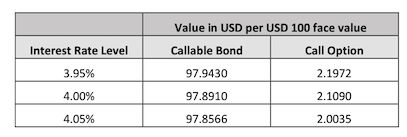

From the table provided, the price of the bond with no embedded options at a 4.00% interest rate is the sum of the callable bond price and the call option price, which is . At a 4.05% interest rate, the price is . The change in price is , and the change in yield is or 10 basis points.

Plugging these values into the formula gives:

This calculation shows that the Dv01 of the bond is 0.02801, which corresponds to option D. The other options (A, B, and C) are incorrect as they do not accurately reflect the calculation of Dv01 using the provided data and the correct methodology.

Ultimate access to all questions.

A risk manager is evaluating the price sensitivity of an investment‑grade callable bond using the firm’s valuation system. The table below presents information on the bond as well as on the embedded option. The current interest rate environment is flat at 4%.

The DVO1 of a comparable bond with no embedded options and with the same maturity and coupon rate as the callable bond is closest to:

A

0.00864

B

0.01399

C

0.01402

D

0.02801