Explanation:

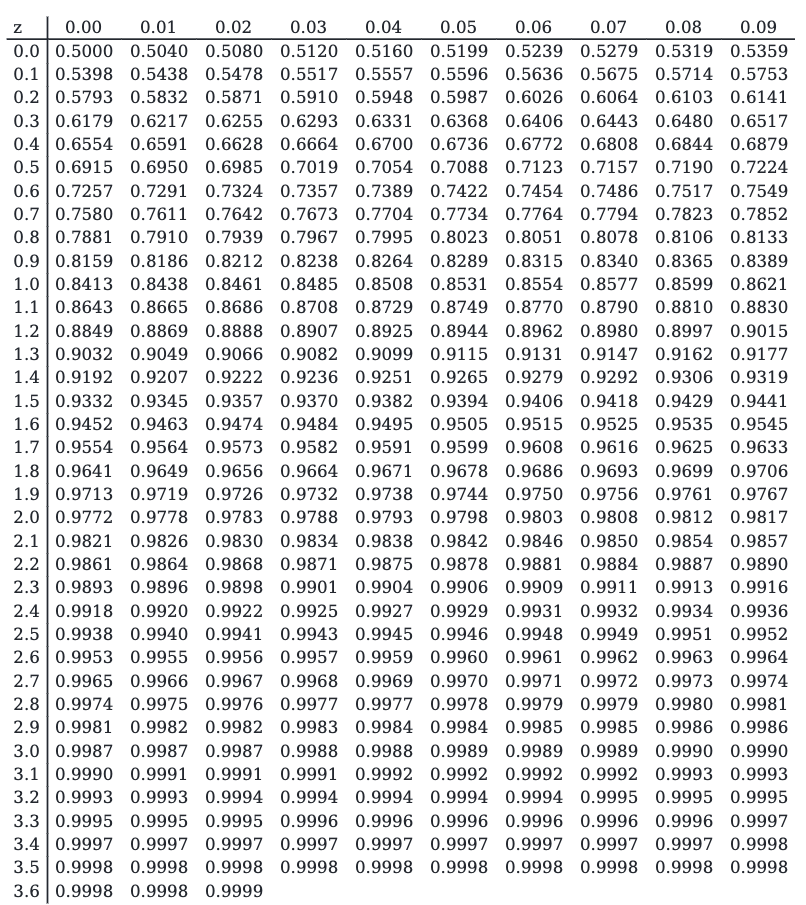

A 16% return is 1 standard deviation above the mean of 9%, since the standard deviation is 7% (9% + 7% = 16%). The probability of getting a result more than 1 standard deviation above the mean is 1 - Prob(Z≤1) = 1 - 0.8413 = 0.1587 or 15.87%. Note: 0.8413 is obtained from the Z-table.

Ultimate access to all questions.

A portfolio has an expected return of 9% with a standard deviation of 7%. If the returns are normally distributed, then what is the probability that the return will be greater than 16%? Click here to view the normal distribution table.

A

0.1052

B

0.2241

C

0.1228

D

0.1587