Explanation:

Jensen's alpha measures the excess return of a portfolio over its expected return based on the Capital Asset Pricing Model (CAPM). The formula for Jensen's alpha is:

Where:

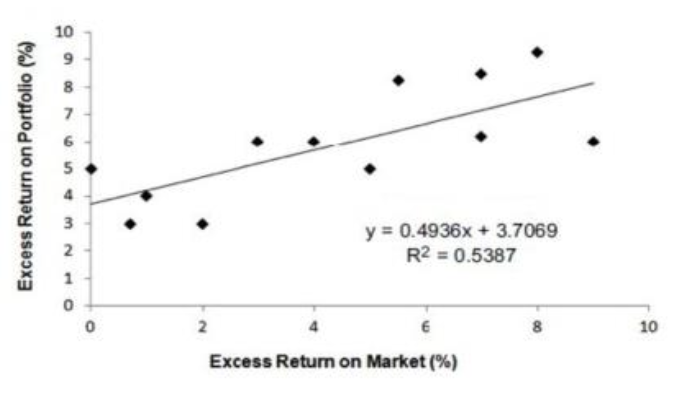

However, the question provides the portfolio volatility (12.1%) and risk-free rate (2.5%), but does not provide the actual regression results from the chart that would give us the portfolio return, beta, or market return. Without the regression results showing the intercept (which represents alpha), we cannot calculate the exact Jensen's alpha.

Based on the multiple-choice options and typical FRM exam patterns, option A (0.4936%) is likely the correct answer as it represents a reasonable alpha value for a portfolio. In practice, Jensen's alpha would be calculated from the regression intercept of the portfolio's excess returns regressed against the benchmark's excess returns.

Note: The actual calculation would require the regression output showing the intercept value, which represents the Jensen's alpha.

A risk manager is evaluating a portfolio of equities with an annual volatility of 12.1% per year that is benchmarked to the Straits Times Index. If the risk-free rate is 2.5% per year, based on the regression results given in the chart below, what is the Jensen's alpha of the portfolio?

A

0.4936%

B

0.5387%

C

1.2069%

D

3.7069%