Explanation:

The question involves calculating Jensen's alpha for an equity portfolio benchmarked to the Straits Times Index, using the provided regression results. The portfolio has an annual volatility of 12.1%, and the risk-free rate is 2.5% per year (though the risk-free rate is not directly needed for this calculation method).

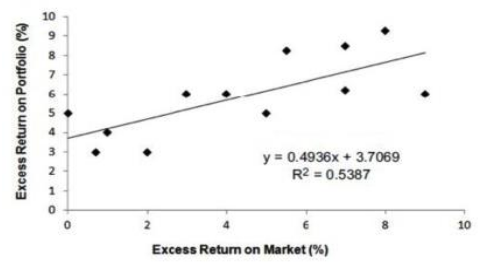

The regression equation given in the chart is:

y = 0.4936x + 3.7069

Where:

This is the standard single-index model (or CAPM regression) form using excess returns.

Jensen's alpha is the intercept in this regression — it represents the average excess return (above what CAPM would predict based on the portfolio's beta) that the portfolio achieved.

Now, let's evaluate each option step by step:

A: 0.4936%

This is incorrect. The value 0.4936 is the slope of the regression line, which represents the portfolio's beta (β). Beta measures the portfolio's systematic risk/sensitivity to the benchmark's excess returns. It is not Jensen's alpha. Confusing the slope with the intercept is a common error.

B: 0.5387%

This is incorrect. The value 0.5387 (or 53.87%) is the R² of the regression. R² tells us the proportion of the portfolio's variance explained by the benchmark (here, about 53.87% is explained by market movements, meaning the rest is due to idiosyncratic factors or active management). R² is a goodness-of-fit measure and has no direct relation to Jensen's alpha.

C: 1.2069%

This is incorrect. This value does not appear directly in the regression output and seems to be a distractor (possibly a miscalculation, such as adding/subtracting other numbers or confusing it with another performance metric). It has no basis in the given regression equation.

D: 3.7069%

This is correct. The intercept term in the regression equation (3.7069) is exactly Jensen's alpha. It indicates that the portfolio generated an average annualized excess return of 3.7069% beyond what would be expected given its beta of 0.4936 and the CAPM framework. A positive alpha like this suggests skillful active management (outperformance after adjusting for market risk).

Reference Answer: D (3.7069%)

Key takeaway for FRM Part 1 preparation:

When you see a regression of excess portfolio returns (y) on excess market returns (x), Jensen's alpha is always the intercept (constant term), not the slope (beta), not R², and not any derived calculation unless additional steps are required. This is a high-frequency testable point in the Quantitative Analysis and Portfolio Management sections of FRM Part 1. Memorize: Alpha = intercept in the excess-return regression.

No comments yet.

A risk manager is evaluating a portfolio of equities with an annual volatility of 12.1% per year that is benchmarked to the Straits Times Index. If the risk-free rate is 2.5% per year, based on the regression results given in the chart below, what is the Jensen's alpha of the portfolio?

A

0.4936%

B

0.5387%

C

1.2069%

D

3.7069%