Explanation:

The correct answer is AR(2) because:

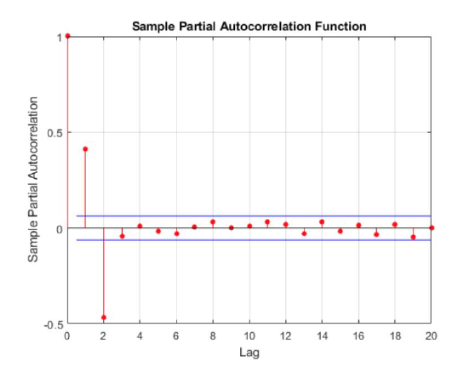

Therefore, the PACF cutting off after the second lag clearly suggests that an AR(2) model is the most appropriate regression approach for this security's time series data.

No comments yet.

A market risk manager would like to analyze and forecast a security performance and has obtained the historical time series for that security. The manager consults a colleague from the quantitative analytic team who provides the following Partial Autocorrelation Function (PACF) plot. Based on the plot above, which of the following is the best regression approach for the security?

A

AR(1)

B

MA(1)

C

AR(2)

D

MA(2)